Rupee erosion, taxes, AI leadership gaps, and stalled manufacturing are making the case for global allocation.

The real question is no longer whether India remains compelling. It’s whether an India-only portfolio is enough.

Most Indian investors still evaluate wealth in rupees. But an increasing share of life goals is effectively linked to global currencies whether it is foreign education, international travel, imported technology, or lifestyle inflation tied to the dollar.

The answer is increasingly clear: Indian investors need at least some of their money working in dollar terms

Six Structural Reasons

Rupee Depreciation

Global Returns

Diversification

AI Supercycle

Manufacturing Gap

Rising Tax Costs

The Return & Diversification Case

02

Reasons 1 through 4 for global allocation

01

The Rupee Quietly Erodes Purchasing Power

The Indian rupee has depreciated against the US dollar by about 3.5% per year on average over the last 20 years. Over a decade or two, this acts like a silent drag on global purchasing power. Owning dollar-denominated assets creates a natural hedge because the currency movement itself boosts the rupee value of the investment over time.

~3.5%

Average annual INR depreciation vs. USD over 20 years a silent but compounding drag on wealth.

02

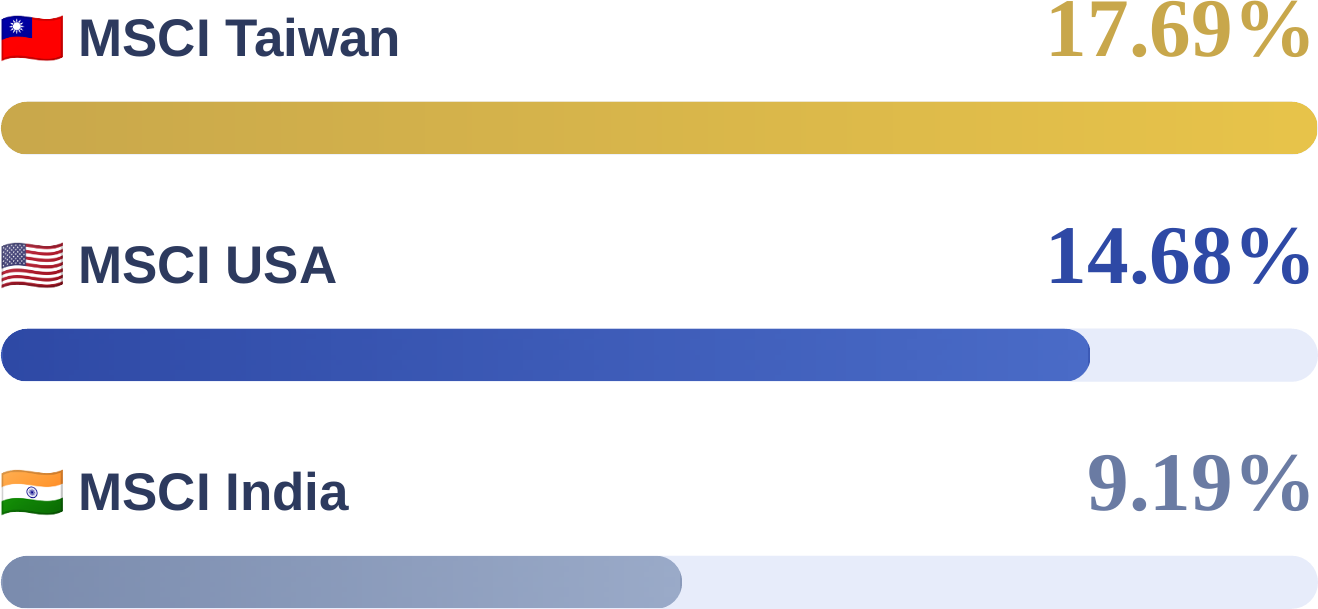

Global Markets Have Compounded Strongly

MSCI USA delivered a 10-year annualized net return of 14.68% in USD terms, while MSCI Taiwan Capped delivered 17.69%. MSCI India delivered 9.19% before considering the additional rupee depreciation benefit.

10-Year Annualized Returns (USD Terms)

MSCI Index Net Returns · Source: MSCI

★ Indian investors receive an additional tailwind from INR depreciation (~3.5% p.a.) when converting USD returns back to rupees.

03

Diversification Is Basic Portfolio Discipline

India accounts for only a small share of global market capitalization, yet most Indian portfolios remain almost entirely exposed to domestic equities. That means investors are making an outsized bet on one country’s valuation cycle, one policy environment, and one macro story.

04

The AI Supercycle Is Being Monetized Elsewhere

The companies monetizing AI at scale cloud providers, chip designers, advanced software firms, and semiconductor leaders are disproportionately listed in the US and Taiwan. Investors who want direct equity exposure to the AI buildout need overseas allocation.

Cloud Providers

Chip Designers

Advanced Software

Semiconductors

Taxes, Manufacturing & the India-Plus Framework

03

Reasons 5 & 6 — and the final conclusion

Manufacturing Value Added (% of GDP)

India’s manufacturing share has not expanded as expected

the ambition hasn’t matched the data.

Reason 5: Taiwan and export-oriented economies built listed corporate champions through deep manufacturing ecosystems. India is still working toward that scale.

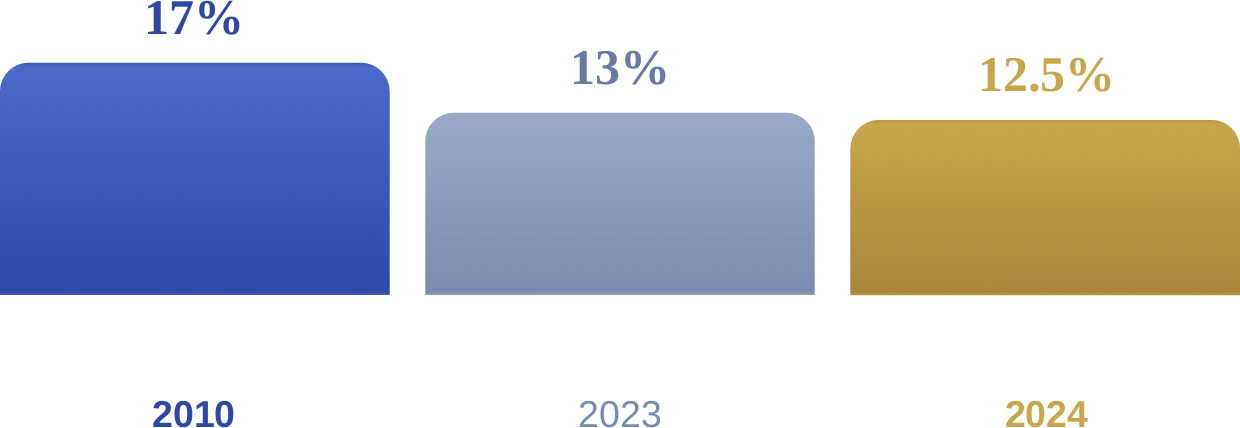

Reason 6 Risingcosts

TAX / COST

RATE

LTCG on Listed Equity

12.5%

STCG on Listed Equity

20%

STT — Equity Delivery

0.1%+0.1%

STT — Futures (from Apr 2026)

0.05%

STT — Options Premium (from Apr 2026)

0.15%

Post July 2024 budget changes. Rising taxes & transaction friction strengthen the case for broader geographic allocation.

The India – Plus Framework

India + World

Not India vs. the world — own both.

Currency Hedge

Dollar assets protect purchasing power as the rupee weakens structurally over time.

Return Potential

US and Taiwan markets have delivered stronger USD compounding over the last decade.

True Diversification

Reduce dependence on one country, one currency, and one policy cycle.

AI & Manufacturing Access

Global markets offer exposure to sectors and ecosystems India is still building toward.

Tax Efficiency Lens

Rising domestic taxes and transaction charges make broader allocation more relevant.

The disciplined investor does not choose between India and the world; the disciplined investor owns both.

by

by  Mutual Funds / Equity PMS

Mutual Funds / Equity PMS NRI – Invest in India

NRI – Invest in India Financial Planning

Financial Planning Legacy Planning / Family Office Solutions

Legacy Planning / Family Office Solutions General Insurance

General Insurance Life Insurance

Life Insurance